Treasury in a PE-backed company means staying liquid, meeting covenant limits, and defending your numbers to sponsors and lenders - under a capital structure with little room for error. For that to work, five workflows need to hold together: cash visibility, a 13-week forecast, covenant monitoring, reconciliation, and reporting. The problem is that most treasury setups don’t meet that standard. If your cash view depends on pulling balances from bank portals and rebuilding your TWCF in Excel, you’re working off delayed information. That works until a payment slips or a receipt lands later than expected - then the numbers stop tying, and you’re left explaining variances you can’t trace.

Why PE-backed company treasury management is different (the 5 structural pressures)

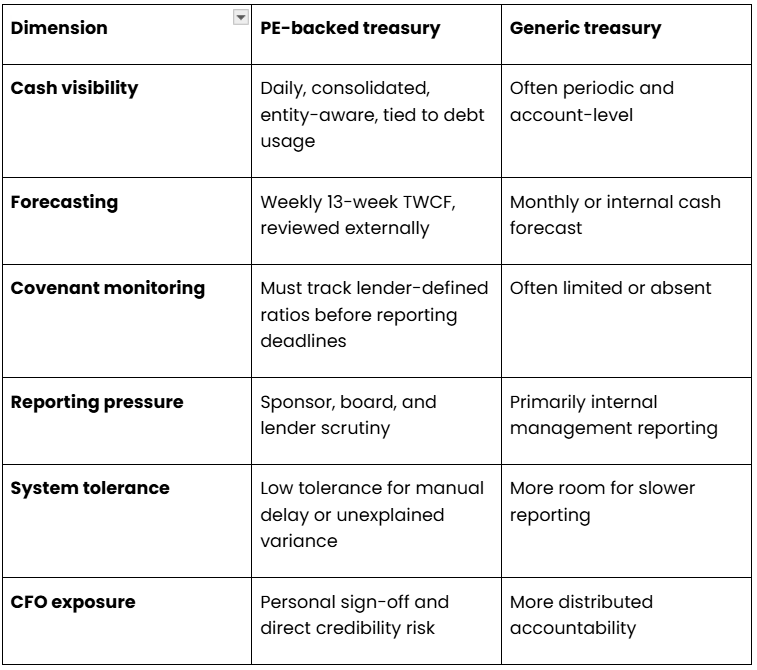

PE-backed treasury runs with leverage in the structure and weekly sponsor scrutiny. When something doesn’t tie out, it gets surfaced quickly - and you’re expected to have an answer. Here’s where that pressure shows up day to day.

1. Leverage changes every cash decision

In a leveraged business, treasury has to be operational. Every dollar you have either protects liquidity, pays down debt, or sits idle while you pay interest somewhere else. If one entity holds excess cash while another is borrowing to fund operations, you’re paying interest unnecessarily. If customer payments come in late by even two weeks, available liquidity tightens, and the impact moves straight into sponsor conversations. What matters is how much usable cash you have to service debt and run the business - by entity and by facility - based on who holds it and what your debt agreements allow you to move.

2. Reporting cadence shifts from monthly to weekly

You’re explaining cash movement continuously. That includes a weekly cash forecast, producing monthly sponsor or board reporting, and delivering quarterly lender reporting - while responding to ad hoc questions whenever results don’t match the plan. If a sponsor asks why week 4 cash collections came in below plan and what that means for your borrowing by month-end, you need an answer quickly. Answers that require manual data pulls or rework point to a broken process that can’t support the reporting cadence.

3. Covenant exposure creates hard thresholds

Covenant pressure doesn’t start when the certificate is due. It builds in the weeks leading up to it. The credit agreement sets EBITDA, not your internal model. If you’re using the wrong definition, you can misstate your covenant position. Add-backs, pro forma adjustments, and timing differences between activity and reporting can shift the outcome further. If you don’t see that early, you’re left reacting with limited options.

4. Multi-entity complexity compounds quickly

Cash can sit in one entity while another draws on the revolver - and you don’t see it until after the fact. That’s because the headline cash number hides how cash is distributed and what you can actually use. Access and movement vary by entity, so a consolidated balance doesn’t tell you whether cash offsets borrowing or supports operations where it’s needed. In a multi-entity setup, you need to see where cash sits, whether it’s accessible, and how it moves across the business - not just how much exists.

5. Accountability is personal

Treasury outcomes are attributed directly to you.

You sign the compliance certificate. You stand behind the forecast. You explain what changed and why, and what happens next.

If confidence in your cash reporting weakens, scrutiny increases across everything. This includes forecast assumptions, EBITDA adjustments, and variance explanations.

That’s why many PE-backed finance teams move beyond spreadsheets to a more controlled setup. Not for better dashboards, but for a system where cash, forecasts, and covenant position stay aligned and don’t need to be rebuilt to explain changes.

Below is a chart breaking down the differences between PE-backed treasury and generic treasury.

The 5 pillars of PE treasury management

Treasury in a PE-backed company is driven by five core workflows. They are tightly linked - when one breaks, the impact carries through the rest. At Nilus, we’ve grouped these workflows into the 5 Pillars of PE Treasury Management - a framework you can use to optimize treasury management for PE portfolio companies.

Pillar 1: Real-time cash visibility

This is the starting point, because every other treasury decision depends on it. In a PE-backed company, the number that matters isn’t total cash. It’s usable cash by entity and account, within the constraints of your debt structure. After an acquisition, that becomes harder to track. Now, cash sits across entities and accounts, some of it restricted, some already committed. At a group level, your cash position can look healthy while the part of the business under pressure has no access to it. The issue isn’t speed. It’s false confidence. A manually consolidated cash report can tie out and still miss where liquidity is tightening, or where cash is sitting idle while debt remains drawn. That’s why same-day visibility needs to show a consolidated view across all entities and bank accounts, with enough detail to separate total cash from available cash and enough context to act on it. If getting there still depends on pulling balances from multiple bank portals, that’s the first issue to fix.

Pillar 2: 13-week cash flow forecast (TWCF)

The 13-week cash flow forecast is where treasury gets tested. It shows whether you’re in control of short-term liquidity and helps sponsors and lenders understand whether pressure comes from timing, deterioration, or a real constraint. When a TWCF breaks, it’s usually because the assumptions don’t reflect how cash actually moves. Collections are modeled on payment expected terms instead of observed behavior, and disbursements follow invoice dates rather than actual payment timing. Key outflows - like payroll, debt service, and taxes - are added too late. When actuals come in, they don’t tie back cleanly, so variance builds without a clear driver. The file gets produced, but nobody really trusts it. Each week, the forecast changes without becoming more reliable. A controlled TWCF is built around how cash behaves in practice. Collections reflect real payment patterns, and disbursements align to actual timing. Fixed obligations are visible upfront, and one-off items are identified early enough to track. Actuals feed back into the model weekly so that any movement can be explained at the line level. This is also where time gets lost. If your TWCF takes hours each week to build, the process is too manual. Your team should focus on testing assumptions and deciding what moves, not rebuilding the file. The forecast should update as inputs change and clearly show what’s most likely to affect your cash position next.

Pillar 3: Covenant compliance monitoring

If covenant tracking happens as part of quarter-end reporting, you’re finding out your position at the same time you’re required to report it. By then, there’s little room to adjust - working capital and cost actions take time, and any conversation with lenders starts from a weaker position. You need visibility earlier, while the outcome can still change. That means tracking covenant positions continuously using lender-defined logic, not internal versions of EBITDA. The mechanics already exist in your credit agreement. The challenge is keeping those definitions inside your day-to-day model. When they sit outside it, covenant position gets calculated separately. And that’s where errors creep in. Headroom can look stable under internal assumptions, then tighten once lender-defined adjustments are applied. The change usually comes from timing, adjustments, and how the ratio is calculated. A controlled setup keeps covenant logic embedded in the same model as your cash and forecast. As inputs change, headroom updates with them, giving you a current view of where you stand and what’s driving it. At any point, you should be able to answer: Where do we stand today under lender definitions? What is most likely to move that position over the next few weeks? If those answers only come together when the certificate is due, you’ve already lost time to act.

Pillar 4: Bank reconciliation and close

Reconciliation ensures the numbers you use are accurate and reliable. When it runs late, close gets compressed, and reporting inherits the volatility. Unresolved items stay mixed into balances already used for cash updates, board reporting, and covenant support. Most of this activity is routine - cash receipts, vendor payments, intercompany transfers - but when it isn’t cleared continuously, it piles up and gets pushed into the close window. That’s when timing differences, misapplied cash, and cutoff issues start to surface - right as reporting is being built. A controlled treasury process moves that work earlier. Routine activity is cleared as it comes in, and exceptions are identified with context while they’re still easy to resolve. By period-end, your team is working through a smaller set of items that actually require their judgment. Close then becomes a confirmation step, not a catch-up exercise - faster, with fewer late adjustments and less pressure on the reporting cycle.

Pillar 5: Sponsor and lender reporting

Reporting is where treasury gets exposed. You’re expected to move from a weekly cash update to a monthly package to a quarterly compliance certificate without changing the underlying story. The issue shows up when those outputs don’t align. When that happens, discussions shift away from liquidity and performance to how the numbers were defined and built. Follow-ups increase, timelines extend, and more time gets spent explaining how the numbers were built. The fix is a reporting process built on a single, governed data foundation, with each output pulling from the same logic. Weekly cash reporting, forecast updates, and covenant support should come from the same inputs and be reviewed in sequence. By the time numbers reach a sponsor or lender, they’ve already been used, tested, and explained internally. This keeps reporting from becoming a separate task each cycle and makes it part of the same process finance already runs.

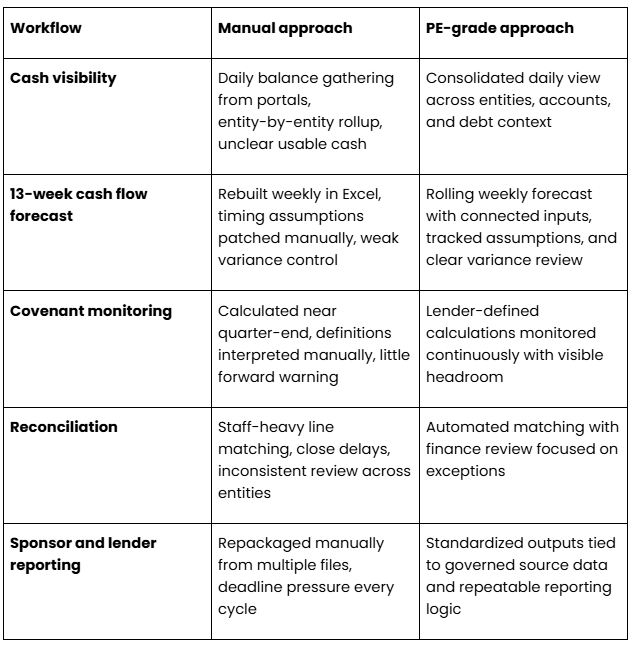

Manual vs. automated approach in a PE-backed treasury function

Read More on Cash Management Software vs. Excel: What’s the Right Tool for Your Business?

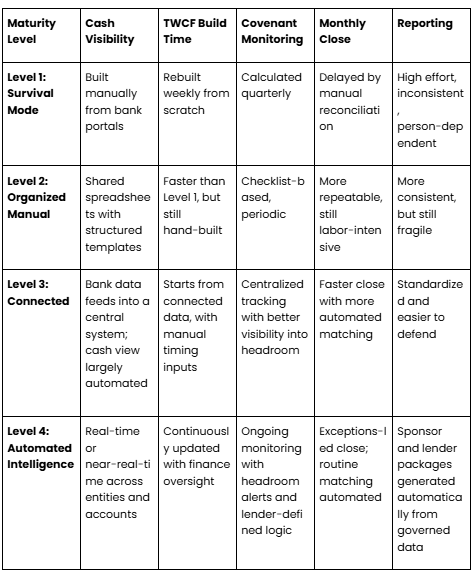

The PE Treasury Maturity Model

Treasury maturity improves as you reduce how much of the process still has to be rebuilt each cycle.

Early on, you can still get the outputs you need - but it takes too much manual work to hold together. As the business grows, that approach breaks.

This model shows how your setup evolves as those workflows become more connected and less dependent on rebuilds.

Level 1: Survival Mode

At Level 1, treasury exists - but only because you keep rebuilding it every cycle. Cash is pulled manually from bank portalsThe TWCF is rebuilt weekly from prior versionsCovenant calculations happen near reporting deadlinesReconciliation is slowClose timing depends on how quickly manual issues are cleared In this setup, you can produce answers, though they take time and rely too much on manual work. As complexity increases through acquisitions, tighter liquidity cycles, or more detailed reporting, the process starts to break in visible ways.

Level 2: Organized Manual

At Level 2, you introduce structure, but the process still depends on manual work at critical points. Shared spreadsheets and standard templates exist for cash and TWCFReporting cadence is definedCovenant tracking follows checklistsReconciliation is more repeatable That structure makes things feel more under control, especially since the process is no longer sitting in one person’s head. But the underlying dependencies haven’t changed. You still pull balances to build your cash view. Forecasts still take time to prepare. Covenant monitoring happens at intervals, not continuously. Reporting is more consistent, but producing it still takes significant effort. So the process works - until something changes.

Level 3: Connected control

At Level 3, treasury starts behaving like a real operating system instead of a workflow you rebuild. Bank data is connected into a central environmentERP inputs feed key cash driversCash visibility becomes consolidated and dailyTWCF starts from connected data, not manual buildsCovenant tracking becomes more centralizedReconciliation relies more on matching logic and less on line-by-line handling As a result, the function stops feeling fragile. You can answer same-day cash questions without delay, and weekly forecast prep shifts from assembling numbers to making decisions. The close starts to move with less friction. You’re not fully automated, but the system is stable enough to hold under PE reporting cadence.

Level 4: Automated intelligence

At Level 4, routine execution no longer depends on your team rebuilding the process each cycle. The system handles it, and your role shifts to control. TWCF updates from connected inputs and highlights movementCovenant logic runs continuously under lender-defined calculationsTightening headroom is flagged ahead of reporting cyclesReconciliation clears routine activity automatically and surfaces only exceptions for reviewReporting packages are generated from governed data Note that you’re not stepping away from treasury. You’re still setting assumptions, defining thresholds, and reviewing outputs. But now the system handles the repetitive work that used to absorb your team’s time. Your effort shifts to decisions, exceptions, and risk. That’s what maturity looks like in a PE-backed company: not more dashboards, but less reliance on manual effort in the workflows your sponsors and lenders depend on.

Where most PE-backed companies are vs. where they should be

Most PE-backed companies stay in Level 1 or Level 2 longer than they should because the process still appears workable. You can get the package out, so it feels like things are holding. That illusion breaks when liquidity tightens or reporting demands increase. At that point, the issue isn’t output - it’s whether the process behind it can keep up. The transition is straightforward. First, connect the workflows, then reduce how much of the process still depends on manual work. Most Nilus customers move from Level 1 to Level 4 in under 90 days. Start your assessment, or read more on Treasury Readiness Quiz: Is Your Treasury Team Prepared for the Future?

Common PE treasury mistakes (and how to avoid them)

Covenant monitoring only at quarter-end

If you wait until quarter-end to run the covenant ratio, you’ve already lost time you may need to respond. By then, options are limited and any fix has to be made within the reporting window. The better approach is to monitor headroom throughout the quarter using lender definitions. That gives you time to see movement early and act before results are locked in.

Using accounting EBITDA instead of lender-defined EBITDA

The EBITDA used for management reporting rarely matches what the lender tests. Add-backs, pro forma adjustments, and definition differences can materially change the ratio. The fix is to build your covenant model directly from the credit agreement and update it alongside your operating data. Otherwise, headroom will appear stronger than it is.

Building the TWCF in isolation

A TWCF built only by finance tends to look clean on paper, but doesn’t reflect how cash actually moves. That’s because timing sits with different teams. Collections timing sits with sales and AR. Payment timing sits with AP. Payroll sits with HR or payroll ops. When those inputs don’t come in directly, you’re filling the gaps with assumptions. The forecast gets stronger when finance owns the model and operating teams provide the timing inputs.

Not consolidating cash across entities

This is a common way value leaks in a roll-up. You’re looking at total cash, but one entity is sitting on excess while another is borrowing to fund operations. It comes down to where cash sits, whether you can move, and whether one part of the business is borrowing while another sits idle. If $1 million is unused in one entity while another borrows at 8%, that’s about $80,000 a year in avoidable interest. To avoid that, you need a daily view of cash by entity and account, with clear visibility into restrictions and movement. That’s what allows you to reduce unnecessary borrowing.

Treating sponsor reporting as a chore, not a trust-builder

When you treat reporting as a separate task each cycle, the numbers stop matching across cash, forecast, and covenant views. To fix that, standardize the package. Use the same structure each time, keep a clear cash bridge, and prepare support schedules the same way every cycle so the numbers carry through.

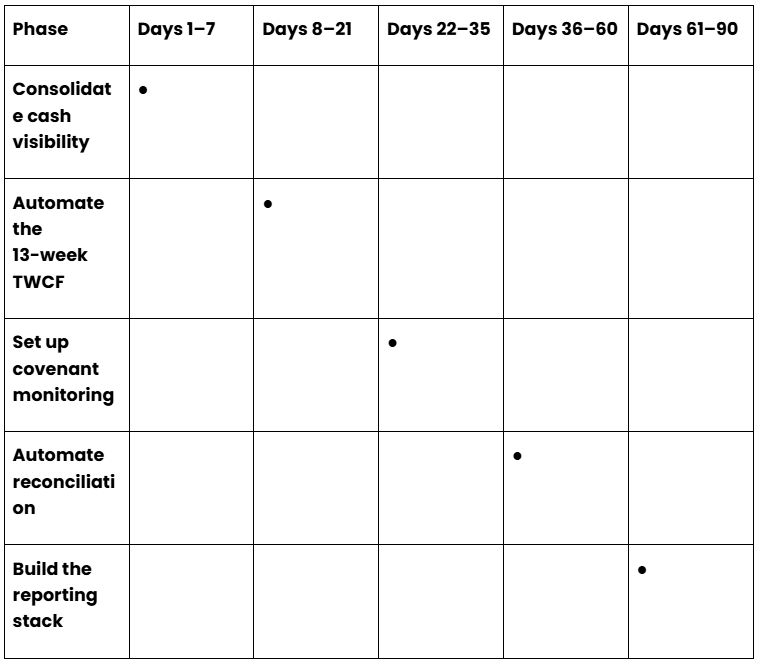

How to build a PE-grade treasury operation in 90 days

Many PE-backed companies try to improve reporting before fixing the workflows underneath it. That gives you a cleaner package without improving how treasury runs.

The fastest way to improve treasury is to fix the workflows in the order they depend on one another. Start with cash visibility, then build the 13-week cash flow forecast, then layer in covenant monitoring, reconciliation, and finally reporting. Each phase makes the next one more reliable.

Here’s a 90-day plan to build a PE-grade treasury operation:

Days 1–7: Consolidate cash visibility

In the first week, focus on building a same-day cash position you can trust. Connect every bank account into one platform and confirm the account list is complete before using the output. Missing smaller or legacy accounts is the most common failure here - and it directly affects the answer you give. By day 7, if someone asks where liquidity stands today, you should be able to answer without pulling bank portals, consolidating balances manually, or following up later.

Days 8–21: Automate the 13-week TWCF

This is where you move from reporting cash to managing it. Connect the inputs that drive near-term liquidity: AR, AP, payroll, debt service, rent, taxes, and known one-off items. Assign clear owners for each assumption. You should own the forecast structure and weekly variance review, while collections, payments, and payroll should come from the teams closest to them. Don’t confuse data access with automation. Pulling ERP balances into a dashboard doesn’t give you a usable TWCF. The forecast only becomes credible when it reflects real timing, updates with actuals each week, and explains movement without rebuilds.

Days 22–35: Set up covenant monitoring

Pull every active covenant from each credit agreement into a controlled model. Use the actual lender definitions, testing dates, add-backs, pro forma adjustments, cure provisions, and reporting deadlines. Remember, internal EBITDA and lender-defined EBITDA aren’t the same. If you track covenant position off the wrong definition, headroom will look stronger than it is. Once that logic is built into the model, set alert thresholds to monitor headroom continuously.

Days 36–60: Automate reconciliation

This is where you start getting time back. Once your bank and ERP feeds are connected, start with the highest-volume transaction categories: customer receipts, payroll, vendor payments, debt service, and standard intercompany activity. Leave edge cases for later. Also, build matching rules that clear routine activity and surface exceptions quickly. If match rates stay low, fix the inputs - mapping, reference fields, or transaction categories that are still inconsistent.

Days 61–90: Build the reporting stack

Now turn treasury into a repeatable reporting process. Use a consistent weekly sponsor package. It should include a 13-week forecast view, cash bridge, commentary on material movement, and a short liquidity or covenant update when needed. Then carry that same logic into monthly cash reporting and quarterly lender support. Also, keep all reporting support in one place - covenant definitions, past forecast versions, supporting schedules, source files, and templates. By day 90, your team should not be pulling from scattered files or rebuilding context each time.

What should be different by day 90

If the plan is working, you’ll feel the difference in how private equity treasury operations run. The process should feel materially less reactive. Cash visibility no longer depends on portal work. Your TWCF is easier to update and defend. Covenant movement surfaces earlier, and close stops absorbing routine reconciliation work. Start your PE treasury transformation - Book a 30-min demo tailored for PE-backed CFOs.

What to look for in treasury software for PE-backed companies

When evaluating the best treasury software for private equity, features aren’t the differentiator. Every system shows cash, forecasts, and reports. What matters is whether it removes manual dependency from the workflows your team relies on. That shows up in how the system performs day to day:

1. Fast deployment with usable output early

You need a working cash position and a usable 13-week forecast within weeks. If implementation runs long, your team stays in spreadsheets while reporting pressure increases. Bank data should flow in directly, and the forecast should run on a pre-built structure from day one.

2. Operable by finance without IT dependency

When payment timing changes or a new entity is added, your team should be able to update logic and maintain integrations themselves. If changes require support, they get delayed or handled outside the system - and that’s when numbers stop lining up across reports.

3. Native covenant monitoring using lender definitions

Covenant tracking should sit inside the same model your team uses every day. When it’s separate, headroom gets checked too late. EBITDA definitions, add-backs, and adjustments should follow lender terms and update automatically as inputs change.

4. A 13-week forecast that reflects timing, not just balances

The system should be able to maintain the forecast without requiring finance to rebuild timing assumptions every week. Actuals should feed back automatically, and changes in AR, AP, payroll, or scheduled cash events should flow through without manual adjustment. When numbers shift, you should see what changed and why.

5. Built-in multi-entity consolidation

Your cash position should be consolidated across entities and accounts by default. If consolidation depends on exports or manual alignment, you’re working with a delayed view. You should be able to move between entity-level detail and a consolidated position without breaking either.

6. Execution built into the workflow

The workflow shouldn’t stall when a data feed is late or an input is missing. The system should surface the gap, continue processing what’s available, and isolate exceptions. Routine matching and updates should run automatically so your team can focus on exceptions, not maintenance.

7. Pricing aligned with a PE-backed operating model

The system should reduce ongoing manual work, not add implementation overhead or require dedicated resources to maintain. If it takes months to stabilize or requires constant support, it doesn’t fit a PE-backed operating model. See how Nilus supports these 7 workflows in a live demo built for PE-backed CFOs.

Frequently Asked Questions About PE Treasury Management

What is treasury management for PE-backed companies?

Treasury management in a PE-backed company is how you manage cash, debt, and reporting to meet sponsor and lender expectations. That involves maintaining a current view of cash across entities, running a 13-week forecast you can stand behind, and tracking covenant headroom before it tightens. If any part of that depends on delayed or manual processes, issues tend to surface in sponsor discussions or covenant reporting. With leverage in the structure, those issues escalate quickly. A delay in cash, a miss in the forecast, or a mismatch in reporting carries through to borrowing and covenant position - and you’re expected to explain it immediately.

What treasury software is best for PE-backed companies?

The best treasury software for PE-backed companies is the one that reduces manual work in the core workflows - cash visibility, forecasting, covenant tracking, and reporting - while remaining operable by a lean finance team. Enterprise tools like Kyriba and GTreasury are built for larger teams and longer timelines. In a PE-backed environment, that usually means over-implementation and slow adoption. Purpose-built platforms like Nilus are designed to hold up better because they match how the function actually operates.

How do PE sponsors monitor portfolio company cash?

Through the weekly 13-week cash flow forecast. That’s the core operating rhythm. Each week, you’re expected to walk through what changed, what’s coming, and where pressure is building. Sponsors focus on movement: receipts vs. plan, timing of outflows, revolver usage, and covenant headroom. The numbers matter, but consistency matters more. If your forecast shifts and you can’t explain why, that gets noticed quickly. Learn how to automate your cash flow forecast.

What are the biggest treasury challenges for PE-backed CFOs?

The biggest treasury challenges for PE-backed CFOs are managing cash across entities, keeping forecasts aligned with real timing, and staying ahead of covenant positions under leverage. As complexity increases, small gaps in visibility or timing compound quickly, especially when the process still relies on manual consolidation.

What is the 13-week cash flow forecast for PE companies?

The 13-week cash flow forecast (TWCF) is a rolling weekly projection of expected cash inflows and outflows over the next 90 days. It’s used to track liquidity, explain movement, and anticipate pressure before quarter-end.

How often should a PE-backed company report to its sponsor?

Most PE-backed companies report weekly on cash, monthly on financials, and quarterly for covenant compliance. This cadence gives sponsors a consistent view of liquidity and performance. If reporting only happens at month-end, issues tend to surface late, especially around liquidity and covenants. This ties directly to how covenant compliance is monitored.