Your Controller sends over your monthly cash report, and you start to scroll. You’re reviewing every entity, and then you see it. $3.2 million sitting in the Ohio operating account. Earning 0.05%. You flip to the borrowings tab. The revolver is $4 million at 8.25%. You quickly do the math in your head: the $3.2 million is costing you roughly $264,000 a year. Not in any line item. Not on any board deck. It’s just disappearing. $720 a day. There it goes, into the gap between what that cash is earning and what your debt is costing. And it’s been sitting there for six weeks. Nobody did anything wrong. The Controller maintained a comfortable buffer. The treasury team didn’t have a real-time view across entities. The monthly close caught it the way a monthly close catches everything: 30 days late. This is idle cash. And if you have $25 million or more in aggregate cash across more than a few entities, you probably have it. You just can’t see it yet.

TLDR

Idle cash is money that sits idle. It is in low-yield operating accounts while you pay 6% to 10% on your revolver, or while higher-yield options are available elsewhere. Every $1 million of idle cash can cost $45,000 to $80,000 per year, depending on whether you measure the cost as lost yield or avoidable borrowing cost. Many companies with $25 million or more in aggregate cash may be carrying $2 million to $10 million that they cannot see clearly. In this article, we define idle cash, quantify the cost at your scale, and give you a five-step framework to find it, flag it, and deploy it before the next monthly close.

What Idle Cash Actually Is

Idle cash is not a liquidity problem. It is a visibility problem with a dollar amount attached. The definition is straightforward: cash sitting in a bank account that exceeds the operating minimum for that entity, while earning little or nothing. It could be working somewhere else. But the cost has two components, and most CFOs are only accounting for one of them.

Opportunity cost

An operating account at many commercial banks earns 0% to 0.5% today. A money market fund can earn 4% to 5%. The spread on $1 million, sustained for a year, is $40,000 to $50,000. On $5 million, that is $200,000 to $250,000. None of it shows up on the P&L. It is an invisible yield you never collected.

Borrowing cost

This one is worse.

When Entity A is sitting on $3.2 million in an operating account while Entity B is drawing $4 million on the revolver at 8.25%, you’re paying interest on money you already have.

You’re not just failing to earn yield. You’re paying 8.25% per year to borrow what’s already yours.

That is the double penalty.

Both costs accrue simultaneously, and neither appears anywhere obvious.

Here’s a glimpse at what that looks like:

The Math

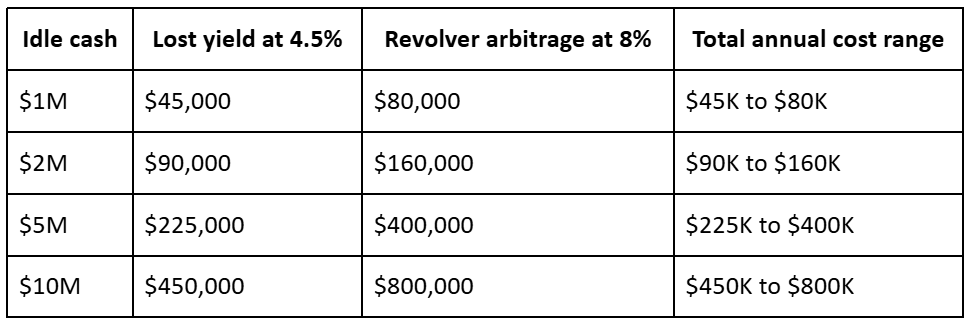

Let’s make those costs more concrete.

The table below shows what idle cash can cost at different balances, based on two scenarios: Yield you’re not capturing, based on a 4.5% spread to a money market fundRevolver arbitrage, based on an 8% cost of debt

In many companies, both are happening at once.

Idle cash is not an accounting quirk. It is a P&L problem you cannot see. And $220 a day, every day, while you sleep, is not abstract. It is the cost of not looking.

So look:

At Nilus, an idle cash optimization program that detects and deploys $2 million at a 4.5% yield can create $90,000 in recovered value in year one. Against a $60,000 Nilus contract, that is a 50% net ROI before counting time savings, risk reduction, or the revolver arbitrage benefit on top. And that assumes you only find $2 million. Many companies find more once every entity account is connected and monitored continuously. Some platforms pay for themselves over time. Nilus can make that payback window much faster when the idle cash opportunity is already present. How much idle cash is hiding in your entities? Find out in a 30-minute demo.

Why Companies Can’t See Their Own Idle Cash

Most finance teams obviously aren’t trying to leave money idle. They simply lack the visibility and mechanisms to act in real time. What looks like a cash optimization problem is often a systems and coordination problem. When you break it down, a few predictable patterns explain why idle cash persists across even the most well-run organizations.

1. Cash is fragmented across entities

A 10-entity company has 30 or more bank accounts. And there’s no single view. The Controller for the Ohio entity knows the Ohio balance. The Controller for the Texas entity knows the Texas balance. Nobody knows both at 9 a.m. on a Tuesday. The CFO gets a consolidated roll-up at month-end, which means the gap between what cash is doing and what it should be doing is measured in weeks, not hours.

2. Operating minimums are set conservatively

Every Controller sets a buffer. It is rational at the entity level, of course. “We keep 60 days of operating expenses in the account, just in case.” Reasonable. But multiply that buffer by 10 entities, and those just-in-case cushions compound into $3 million to $8 million sitting dormant across the organization. Nobody set out to hoard cash. They just never had a system that aggregated the picture.

3. No automated detection

Without real-time monitoring against defined thresholds, excess cash is going to keep sitting there undetected until the monthly close. By then, it has been earning 0.05% for 30 days. The detection is always retrospective. The cost is always already incurred.

4. Intercompany sweeps aren’t automated

Even when you do find idle cash, moving it is filled with friction. Manual wire instructionsIntercompany loan documentationController approvals across time zones The CFO who spotted the Ohio imbalance at 2 p.m. on a Friday is probably not executing a $3 million intercompany transfer before the weekend. The cash sits. Monday arrives. The meter keeps running.

5. The dashboard delusion

Some treasury management systems show you the idle cash. They surface the number. They even put it in a report. But showing you is not the same as fixing the problem. A TMS that tells you $4.2 million is idle at the entity level while you’re paying 8% on the revolver, and then waits for you to do something about it, is not solving the problem. Watching the money burn is not the same as putting out the fire.

The 5-Step Idle Cash Detection and Deployment Framework

The companies that recover idle cash fastest are not doing anything wildly exotic. Rather, they are doing the following five things, in the same order, consistently. And they have real-time data feeding each step.

Step 1: Establish operating minimums per entity

The first thing you’ll do is set a floor for each entity based on 2 to 4 weeks of operating expenses. That floor becomes the threshold. Everything above it is deployable capital. This step sounds administrative because it is. But without it, there is no definition of idle. Every dollar in every account looks necessary because nobody has decided otherwise.

Step 2: Connect all bank accounts for real-time monitoring

Daily visibility is the floor. Real-time is the target. The gap between a daily file feed and a live API connection to your bank is the gap between knowing you had idle cash yesterday and knowing you have it right now. Most idle cash optimization programs fail at this step because they are still running on manual exports.

Step 3: Set idle cash alert thresholds

$100,000 for smaller entities. $500,000 for larger ones. When a balance crosses the threshold, the CFO gets an alert: Entity nameDollar amountHow long it has been above thresholdRecommended action The alert does not ask for a meeting. It does not require a report. It puts the decision in front of the right person, immediately.

Step 4: Define deployment options in priority order

The decision tree is straightforward: If the revolver is drawn and the idle cash rate is below the revolver rate, pay it down. If not, sweep to a money market fund. If intercompany consolidation makes more structural sense, move it to central treasury. The order matters because revolver paydown at 8% beats money market yield at 4.5% every time. Get the math right first, then automate the decision.

Step 5: Automate detection and recommendation

AI agents monitor balances continuously, calculate idle cash by entity in real time, and surface the recommended action with the cost of not acting. The CFO approves. The system executes. This is what separates companies that recover idle cash once from companies that recover it continuously.

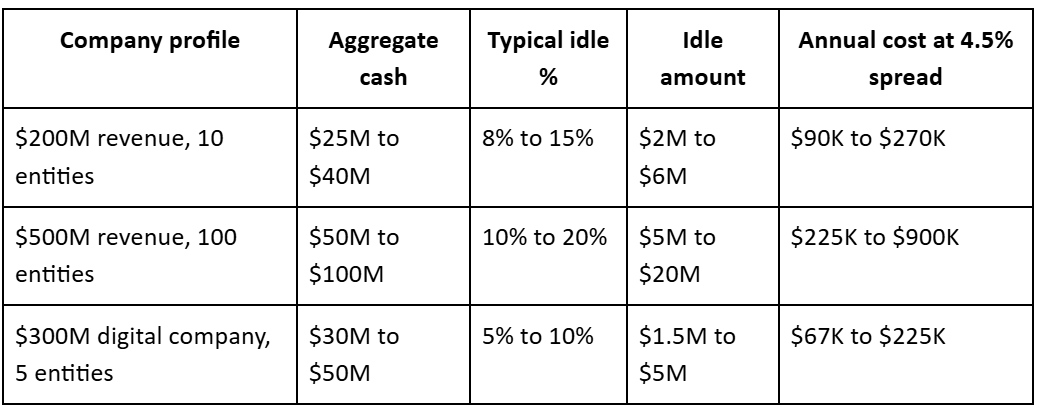

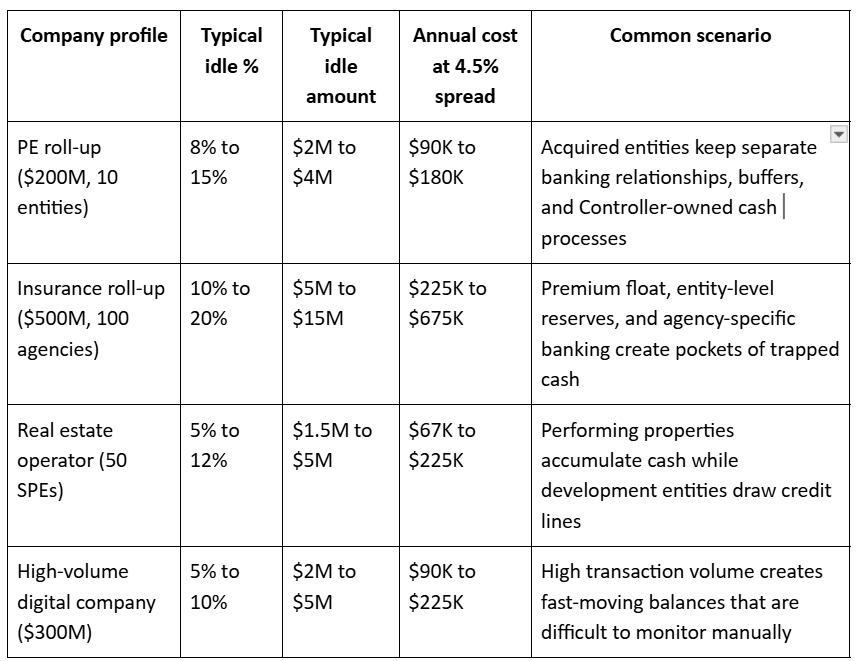

Idle Cash Benchmarks by Company Profile

You cannot uniformly distribute idle cash. The structure of the business determines how much is hiding and where.

Below are the benchmarks we see most often, with the scenario that typically produces them.

PE roll-ups carry the most idle cash in absolute terms. Each acquired entity has its own banking relationships, its own Controller, and its own comfort level with cash buffers. After 5 acquisitions, you have 5 independent cash silos that nobody has aggregated. The idle cash cost compounds with every deal. Insurance agency roll-ups are often worse in percentage terms. Agencies are trained to hold reserves. Premium float creates timing mismatches. A 100-agency platform can have $15 million in idle cash spread across accounts that nobody has connected to a central view. Real estate operators deal with SPE proliferation. Every property is a separate legal entity. Every entity has its own bank account. Cash builds up in performing properties while development entities draw credit lines. The arbitrage between those two states can be millions, invisible to everyone except the person running the monthly entity-by-entity reconciliation. High-volume digital companies move fast and close late. Cash management is not their core competency. The CFO is managing growth, not watching balances. Idle cash accumulates because nobody is watching, not because nobody cares.

What Changes When Idle Cash Becomes Visible

Idle cash optimization is a data problem. When the data is right, the decisions are obvious. When the data is wrong or late, the money disappears quietly. Here’s what good looks like operationally: Every entity bank account is connected via API.Balances update in real time. Operating minimums are set and stored. The system knows, at any moment, exactly how much cash each entity is holding above its floor. Then, when a balance crosses the idle threshold, the CFO gets an alert with the entity name, the idle amount, how many days it has been above threshold, and the recommended deployment action with the dollar value of acting now versus waiting. The deployment logic can then run automatically. If Entity A is sitting on $3.2 million idle while Entity B is drawing the revolver, the system flags the arbitrage and quantifies the daily cost. The CFO can then approve the intercompany transfer, and the wire can go out. The revolver paydown happens that afternoon. At Nilus, our program connects directly to your banks via API, surfaces the consolidated position across every entity in real time, and flags idle cash automatically with a recommended action. The CFO does not have to go looking. The alert finds them. This is the difference between idle cash management as a quarterly exercise and idle cash optimization as a continuous process. One finds the problem in retrospect. The other prevents it from costing you anything.

FAQs

What is idle cash?

Idle cash is money held in a bank account above the operating minimum for that entity, earning little or no return, when it could be deployed to reduce debt or generate yield. For most companies, it is often fragmented across dozens of entity accounts, each individually justifiable. But it is collectively expensive. The cost compounds silently because no single person has the cross-entity view to see it.

How much does idle cash cost?

Every $1 million of idle cash can cost $45,000 to $80,000 per year, depending on whether the comparison is lost yield on a money market fund, roughly 4.5%, or the cost of debt on a drawn revolver, often 6% to 10%. Companies with $25 million in aggregate cash may carry $2 million to $6 million in idle balances, which translates to $90,000 to $270,000 in annual cost. That cost does not appear on any line item. It is the yield you never collected and the interest you paid on money you already had.

How do you detect idle cash in a multi-entity company?

Detection requires three things: A defined operating minimum for each entityReal-time bank connectivity across all accountsAutomated comparison of live balances against those minimums Without the operating minimum, there is no definition of idle. Without real-time connectivity, detection is always retrospective. The companies that find idle cash fastest are the ones that have connected all their bank accounts via API and set entity-level thresholds. These trigger an alert the moment a balance crosses into deployable territory.

What should you do with idle cash?

The deployment decision follows a simple priority order. First, pay down the revolver if the rate exceeds what the cash could earn elsewhere. At 8% on a drawn revolver versus 4.5% in a money market fund, the math favors paydown every time. Second, if the revolver is not drawn or the spread does not justify paydown, sweep idle cash to a money market or short-duration instrument. Third, consolidate to the central treasury if intercompany mechanics make more structural sense than entity-level deployment. The key is to have the decision pre-made, so that when the alert fires, the action is immediate.

How does Nilus help with idle cash optimization?

Nilus connects to your banks via API and surfaces a live consolidated cash position across every entity. It monitors balances against entity-level operating minimums in real time, flags idle cash automatically when a threshold is crossed, and delivers a recommended deployment action with the dollar cost of waiting. For a company carrying $2 million in idle cash, Nilus can help recover $90,000 in yield in year one against a $60,000 contract. The ROI depends on how much deployable idle cash is actually found, but the math becomes visible quickly.

The Alert That Pays for Itself

Back to Ohio.

$3.2 million in the operating account. $4 million drawn on the revolver at 8.25%. $264,000 a year, $720 a day, bleeding out of the business in the gap between what that cash is earning and what the debt is costing.

Nobody noticed for six weeks.

Nobody did anything wrong.

The data just wasn’t there.

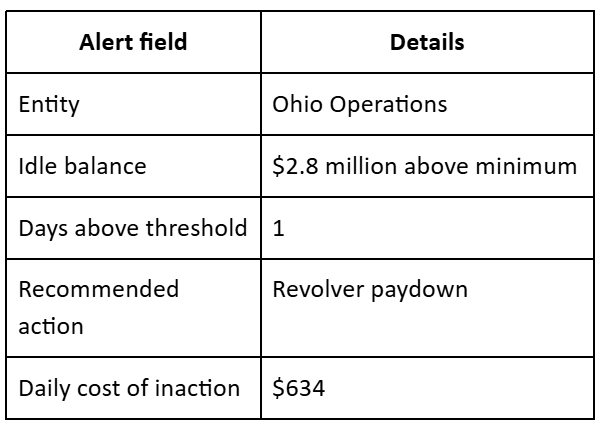

Here is the same scenario with a real-time idle cash monitoring system in place.

The Ohio balance crossed the threshold on a Tuesday morning. The CFO got the alert at 9:14 a.m.:

The CFO approved the transfer by 10 a.m. The wire went out that afternoon. The $264,000 annual cost never happened. That is idle cash optimization. It is a system that watches every balance, every day, and tells you the moment the money starts costing you. The cash was always there. Now you can actually see it and do something about it. Most Nilus customers find $1M to $5M in idle cash within 30 days. Book your assessment today.