Table of Contents

- What Is Covenant Compliance?

- The Most Common Covenant Types (and What CFOs Get Wrong)

- How Covenant Compliance Monitoring Works (The Manual Reality)

- The 4-Layer Covenant Compliance Model

- Covenant Compliance Checklist for PE-Backed CFOs

- How to Automate Covenant Compliance Monitoring

- Covenant Breach: What Happens and How to Respond

- Frequently Asked Questions About Covenant Compliance Covenant compliance is the process of tracking whether your company meets the financial and operational conditions in its credit agreement - and reporting that status to your lender on a defined schedule. For PE-backed companies carrying 1–5x leverage, missing a covenant test doesn’t just trigger a fee. It constitutes technical default, which can accelerate debt repayment, impose restrictions on operations, or give your lender board-level veto rights. Most PE-backed CFOs are tracking covenants manually, in spreadsheets, across quarterly reporting cycles. The process takes 8-16 hours per reporting period. Definitions change between facilities. And there’s no early warning - the CFO discovers they’re close to a breach at the end of the calculation, not the beginning. This playbook covers what covenants are, how to build a monitoring system that flags headroom erosion in real time, and how to use automation to stay permanently ahead of your lender’s reporting requirements. Not a single competitor in treasury technology - Kyriba, GTreasury, Trovata, Agicap, or Atlar - has published meaningful content on this topic. That gap tells you something about where the industry’s attention has been. It hasn’t been on the thing PE-backed CFOs actually lose sleep over.

What Is Covenant Compliance?

Covenant compliance is the ongoing process of monitoring and reporting whether a borrower meets the financial and operational conditions stipulated in their credit agreement. For PE-backed companies, this means tracking specific financial ratios - leverage, interest coverage, minimum liquidity - against thresholds defined by the lender, on a schedule the lender dictates.

There are two primary categories. Financial covenants are ratio-based tests: leverage ratio (Net Debt / EBITDA), interest coverage ratio (EBITDA / Interest Expense), minimum liquidity, and EBITDA floors. Maintenance covenants require ongoing operational compliance - maintaining insurance, filing taxes on time, limiting additional indebtedness. A third category, incurrence covenants, are triggered only when the borrower takes a specific action, such as making an acquisition or paying a dividend.

Why it matters at the level it does: non-compliance constitutes technical default even if the company has adequate cash flow. Lenders can accelerate debt, impose operating restrictions, or require an equity cure from the PE sponsor. According to the Association for Financial Professionals (AFP), covenant monitoring is one of the highest-stakes recurring obligations in corporate treasury - and one of the most under-automated.

Typical reporting cadence depends on the credit agreement: monthly (common in ABL facilities or elevated-risk situations), quarterly (standard for term loans), or annually (audited financial statements). Specific dates are defined in the credit agreement, usually 45-60 days after period-end.

The Most Common Covenant Types (and What CFOs Get Wrong)

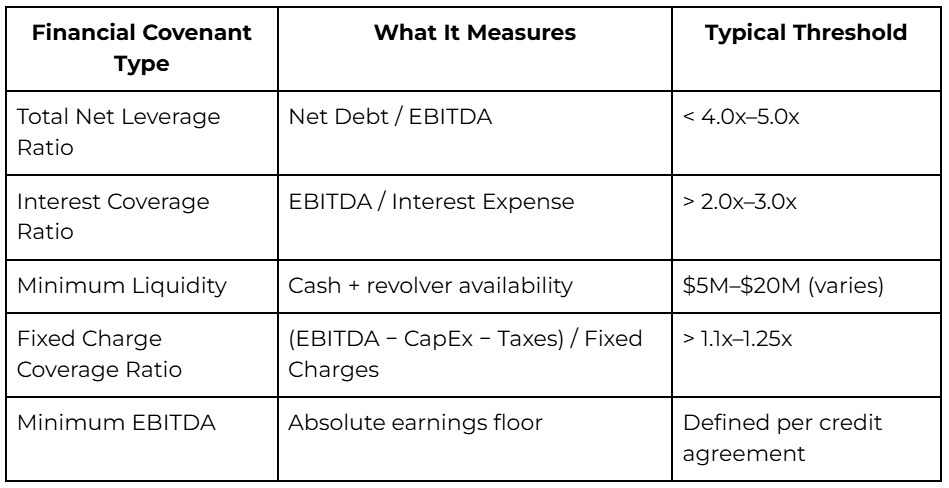

Total Net Leverage Ratio

The most common covenant in PE-backed credit agreements. Calculated as Net Debt divided by EBITDA - but the EBITDA that matters is the lender-defined version, not accounting EBITDA. Typical threshold: below 4.0x–5.0x, depending on the credit agreement and the leverage profile at closing. The ratio is typically measured on a last-twelve-months (LTM) basis. Every quarterly reporting period, the denominator rolls forward. A strong Q1 that drops off the LTM window can push leverage up without any change in operations. This rolling window effect is one of the most common sources of surprise covenant pressure.

Interest Coverage Ratio

EBITDA divided by Interest Expense. This ratio ensures the company’s cash flow covers its debt service obligation. Typical threshold: above 2.0x–3.0x. For companies with variable-rate debt - which describes most PE-backed borrowers in a rising-rate environment - the denominator can shift quarter over quarter without any operational change. Monitoring this ratio monthly, not just quarterly, is the difference between a planned response and an emergency one.

Minimum Liquidity Covenant

Requires maintaining a minimum level of cash or revolver availability. Common in growth-stage PE-backed companies and companies with elevated operating risk. The trap: liquidity covenants are often tested on a spot basis (the exact balance on a specific day), not an average. One bad day can trigger a breach.

Fixed Charge Coverage Ratio (FCCR)

Common in asset-based lending (ABL) facilities. Calculated as (EBITDA minus CapEx minus Taxes) divided by Fixed Charges. More restrictive than interest coverage because it includes all fixed obligations. CFOs managing ABL facilities need to track this ratio separately from leverage - and the definitions rarely align.

Minimum EBITDA

An absolute floor on earnings performance. Less common than ratio-based covenants but frequently included as a backstop in credit agreements for companies with variable revenue. A company can be compliant on leverage but breach minimum EBITDA if the threshold is set above the current run rate.

What CFOs Get Wrong

- Using accounting EBITDA instead of lender-defined EBITDA. Add-backs matter. Management fees, one-time restructuring costs, stock-based compensation, acquisition expenses - the credit agreement specifies which items the lender agrees to exclude. Using the wrong EBITDA definition is the most common compliance error. A company can be in breach on GAAP EBITDA but compliant on lender-defined EBITDA, or vice versa.

- Not tracking the look-back period correctly. LTM calculations roll forward every quarter. A strong quarter dropping off the trailing twelve months can tighten leverage without any operational deterioration. CFOs who calculate ratios only at quarter-end miss the inflection point.

- Missing the cure mechanism window. Most credit agreements include an equity cure provision - the PE sponsor can inject equity to fix a leverage breach. But cure windows are time-limited (typically 10-15 business days after the compliance certificate due date). Missing the window turns a curable breach into an Event of Default.

- Not flagging headroom. Knowing you’re at 4.2x leverage versus a 4.0x limit before quarter-end gives you time to act. Discovering it at step four of the compliance certificate process does not. Headroom monitoring - not just ratio calculation - is the gap in most manual processes.

How Covenant Compliance Monitoring Works (The Manual Reality)

This is the process most PE-backed CFOs follow today. It works until it doesn’t - and when it fails, the failure mode is an Event of Default.

- Pull financial data from the ERP. Export trial balance, revenue, and expense data from QuickBooks, NetSuite, or Sage. Confirm the period is closed. Reconcile any open items.

- Manually calculate covenant metrics in Excel. Build the leverage ratio, interest coverage, FCCR, and any other required ratios from the exported data. Apply the lender’s specific formulas.

- Cross-reference definitions in the credit agreement. Open the credit agreement - often a 200+ page document - and confirm the exact EBITDA definition, add-back schedule, and measurement basis. Definitions are frequently buried in schedules or amendment riders.

- Reconcile to lender-defined EBITDA. Adjust accounting EBITDA for the specific add-backs the lender agreed to. This step alone can take 2-4 hours for a company with multiple adjustments.

- Build the compliance certificate in Excel. Populate the lender’s template with the calculated ratios, supporting schedules, and narrative explanations for any material variances.

- Review with the CEO or CFO. The compliance certificate is a personal attestation. The signer is certifying accuracy. Review typically involves 1-2 rounds of revision.

- Submit to the lender by the required date. Upload or email the compliance package. Hope nothing was missed.

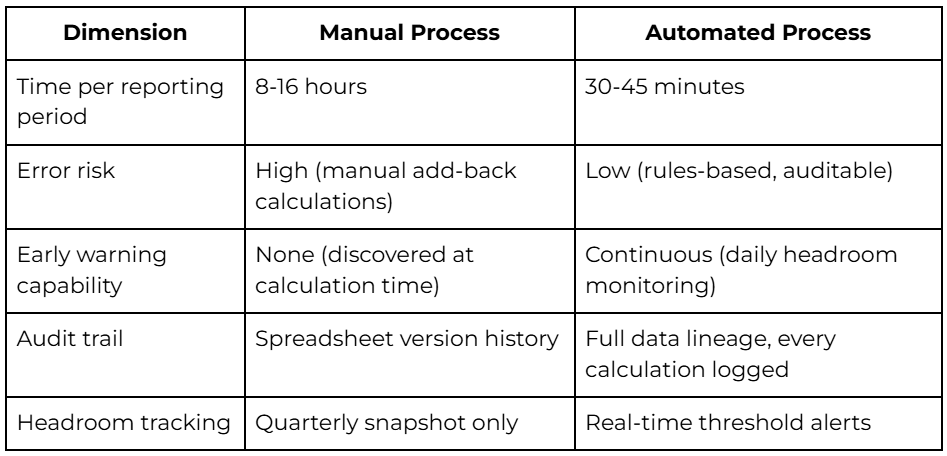

The problem is structural, not just operational. Steps 1 through 4 consume 8-16 hours per reporting period. Add-back calculations are prone to error - one misclassified expense changes the ratio. Definitions change between facilities for companies with multiple credit agreements. And there is no early warning system. The CFO finds out they’re close to a breach at step 4, not step 1.

For the 89 days between quarterly compliance certificates, the CFO has no visibility into where covenant ratios actually stand. That’s flying blind across 97% of the year.

The 4-Layer Covenant Compliance Model

This is the framework for moving from quarterly spreadsheet exercises to continuous, automated covenant monitoring. Each layer builds on the one below it.

Layer 1: Covenant Registry

A single source of truth for every covenant in every facility. This is the foundation. The registry captures: covenant type, threshold, reporting frequency, measurement date, lender name, EBITDA definition (including specific add-backs), look-back period, and cure mechanism details. Most PE-backed companies with multiple credit facilities have no centralized covenant registry. Definitions live in different credit agreements. Thresholds were negotiated at different times. Amendment riders have modified original terms. Layer 1 consolidates all of this into one structured repository.

Layer 2: Financial Data Pipeline

Automated ingestion of ERP, bank, and billing data. No manual exports. No copy-paste from QuickBooks to Excel. The critical capability at this layer is calculating lender-defined EBITDA automatically using saved add-back rules. Each credit agreement has its own EBITDA definition. Layer 2 maintains the specific adjustment rules for each facility and applies them to the incoming financial data without manual intervention.

Layer 3: Headroom Monitoring

Real-time calculation of covenant headroom - the distance between the current ratio and the covenant limit. This is the layer that transforms covenant monitoring from a retrospective exercise into a forward-looking one. Alert thresholds are set at meaningful intervals: flag at 80% of the covenant limit (early awareness), escalate at 90% (planning window), and alarm at 95% (action required). For a leverage covenant of 4.0x, that means alerts at 3.2x, 3.6x, and 3.8x respectively. Headroom monitoring runs daily - or more frequently when ratios are tightening. The CFO knows the current position every morning, not once per quarter.

Layer 4: Compliance Reporting

Automated generation of the compliance certificate, supporting schedules, and the full lender reporting package. Every number in the certificate traces back to its source data through a complete audit trail. Layer 4 also includes the lender data room: a single access point where the lender (or the PE sponsor’s operating team) can review supporting data for every calculation. No ad hoc requests. No “can you send me the backup for the leverage calculation” emails.

Covenant Compliance Checklist for PE-Backed CFOs

This is the 10-point checklist for PE-backed finance teams managing covenant obligations. Use it as a quarterly review framework or as the starting point for building a permanent monitoring system.

- List every facility and its covenants in one place. Capture the covenant name, threshold, reporting frequency, measurement basis (LTM, quarterly, spot), and the specific credit agreement section where it’s defined.

- Confirm the lender-defined EBITDA definition for each facility. Document every agreed add-back and exclusion. If you have multiple facilities, map where the definitions differ. This is the single highest-value step in the checklist - more compliance errors originate here than anywhere else.

- Set calendar reminders for every reporting date - plus a 5-business-day internal deadline before it. The compliance certificate due date is the lender’s deadline. Your deadline is five days earlier. Build the buffer into the calendar, not the process.

- Build or configure headroom monitoring. Flag when headroom drops below 20% of the covenant limit. If your leverage covenant is 4.0x, you want to know when you cross 3.2x - not when you’re at 3.95x.

- Designate a single owner for each covenant. Usually the CFO or Controller. One person is accountable for the accuracy of each ratio. No shared ownership on a personal attestation document.

- Document your equity cure mechanism and timeline for each facility. Know the cure window (typically 10–15 business days after the compliance certificate due date), the maximum number of cures allowed over the life of the facility, and the mechanics of the equity injection.

- Run a quarterly stress test. Answer this question every quarter: “What happens to our covenants if revenue drops 10%?” If the answer is “we breach,” you need a contingency plan before you need a waiver.

- Maintain a compliance certificate template approved by lender counsel. Don’t rebuild the certificate from scratch each quarter. Use a template that the lender has previously accepted. Reduce formatting risk.

- Build an audit trail for all calculations. Lenders can and do request supporting data. Every add-back, every adjustment, every input should trace to a source document. Spreadsheets with hardcoded numbers fail this test.

- Review covenants at every board meeting - not just at reporting time. Covenant headroom is a board-level metric. If your board only sees covenant data quarterly, they can’t help you plan around tightening headroom.

How to Automate Covenant Compliance Monitoring

Moving from manual calculation to automated monitoring follows a defined sequence. Here’s the process:

- Connect your financial data sources. Link your ERP (NetSuite, QuickBooks, Sage), bank accounts, and any off-system revenue data. This eliminates the manual export step - the one that consumes the first 2–3 hours of every compliance cycle.

- Define your lender-defined EBITDA. Configure the specific add-backs, exclusions, and the LTM calculation window for each credit facility. Save these rules so they apply automatically to every future calculation.

- Input your covenant registry. Enter each covenant: name, type, threshold, reporting frequency, measurement date, and cure mechanism. This becomes the structured source of truth that replaces the scattered credit agreement references.

- Set headroom alert thresholds. Configure alerts at 80%, 90%, and 95% of each covenant limit. Assign alert recipients - CFO, Controller, and (optionally) the PE sponsor’s operating partner.

- Configure automated reporting. Set the system to auto-generate the compliance certificate and supporting schedules on the internal deadline (5 days before the lender’s due date). Include the full calculation audit trail.

- Set up the lender data room. Create a single access point where supporting data for every covenant calculation is available for lender or sponsor review - without ad hoc requests or manual data pulls.

Nilus handles all six steps automatically once your data sources are connected. The covenant registry, headroom monitoring, and compliance certificate generation are built into the platform. Finance teams we work with report that covenant monitoring shifts from quarterly manual → daily automated, and the compliance certificate process compresses from 8–16 hours to under 45 minutes. Most PE-backed companies using Nilus are live within two weeks - not the 6–18 months typical of legacy treasury management systems.

Covenant Breach: What Happens and How to Respond

A covenant breach is not automatically catastrophic - but the response window is narrow and the stakes are real. Here’s what happens and what to do about it.

The Breach Triggers a Cure Period

When a covenant ratio misses its threshold, the credit agreement typically provides a cure period of 30–60 days. During this window, the borrower has defined options to resolve the breach.

The Three Cure Mechanisms

- Equity cure. The PE sponsor injects equity into the company to improve the covenant ratio. For a leverage breach, the equity injection reduces net debt. Most credit agreements limit the number of equity cures available over the life of the facility (typically 2–3) and require the injection within a specific window (10–15 business days after the compliance certificate due date).

- Waiver request. The borrower asks the lender to waive the breach for the current period. Waivers are discretionary - the lender is not obligated to grant one. They’re most likely when the breach is narrow, the borrower has a credible plan to return to compliance, and the relationship is strong.

- Amendment. The borrower and lender agree to modify the covenant threshold going forward. Amendments typically involve a fee (0.25%-0.50% of the facility) and may include tighter terms on other covenants or additional reporting requirements.

How to Communicate with Your Lender

The three things lenders want to see when headroom is thinning:

- You identified the issue early. Not at the compliance certificate deadline - weeks before. Early identification signals operational control.

- You have a plan. A specific, credible path back to compliance with a defined timeline. Lenders evaluate the plan’s realism, not its optimism.

- You have the data to support it. A financial model showing the path back to compliance, supported by source data the lender can verify. This is where an audit trail matters most.

Proactive communication is always superior to reactive disclosure. A CFO who calls the lender three weeks before a potential breach with a plan and supporting data gets a fundamentally different response than a CFO who submits a non-compliant certificate on the due date.

FAQs

What is covenant compliance in finance?

Covenant compliance is the ongoing process of ensuring a borrower meets the financial and operational conditions in their credit agreement. For PE-backed companies, this typically means maintaining financial ratios like leverage (Net Debt / EBITDA) and interest coverage (EBITDA / Interest Expense), plus operational requirements like minimum liquidity. Breaching a covenant - even without a cash crisis - constitutes technical default that can give the lender remedies including debt acceleration.

How often do PE-backed companies need to report on covenants?

Most credit agreements require quarterly covenant compliance certificates, delivered 45–60 days after period-end. Some facilities - particularly ABL structures or companies with elevated risk profiles - require monthly reporting. Annual audited financial statements are also typically required. The specific dates and deadlines are defined in the credit agreement and are non-negotiable.

What happens if a PE-backed company breaches a covenant?

A breach triggers technical default, which initiates a cure period (typically 30–60 days). During this window, the borrower can cure the breach through equity injection from the PE sponsor, negotiate a waiver, or amend the credit agreement. If the breach goes uncured, the lender gains remedies including the ability to accelerate repayment. Most breaches are resolved through waiver or amendment when identified and communicated early.

What’s the difference between a financial covenant and a maintenance covenant?

Financial covenants are ratio-based tests - leverage, interest coverage, minimum EBITDA - measured at specific dates defined in the credit agreement. Maintenance covenants are ongoing operational requirements: maintaining insurance, filing taxes, limiting additional indebtedness. Incurrence covenants are a third category, triggered only when the borrower takes a specific action like making an acquisition or paying a dividend above a threshold.

How do you track covenant compliance without dedicated software?

Without dedicated software, most PE-backed CFOs use Excel models, ERP exports, and calendar reminders. The process consumes 8-16 hours per reporting period and requires manual reconciliation of financial data against lender-defined definitions. The primary risks are calculation errors in add-back schedules, missed reporting deadlines, and the absence of early warning when headroom narrows. For the 89 days between quarterly certificates, the CFO has no visibility into current covenant ratios.

What is lender-defined EBITDA and why does it matter?

Lender-defined EBITDA is the adjusted EBITDA specified in the credit agreement for calculating covenant ratios. It differs from GAAP EBITDA by adding back items the lender agrees to exclude: management fees, one-time restructuring expenses, stock-based compensation, and acquisition costs. Using the wrong EBITDA definition is the most common compliance calculation error - a company can be in breach on GAAP EBITDA but compliant on lender-defined EBITDA, or the reverse.

How can Nilus help with covenant compliance monitoring?

Nilus automates covenant monitoring by connecting directly to your ERP and bank data, calculating lender-defined EBITDA using your specific add-back rules, and tracking headroom in real time. When headroom drops below configured thresholds, Nilus alerts your team automatically. Compliance certificates and lender reporting packages generate on schedule, with a complete audit trail for every calculation. Most PE-backed companies are live within two weeks.